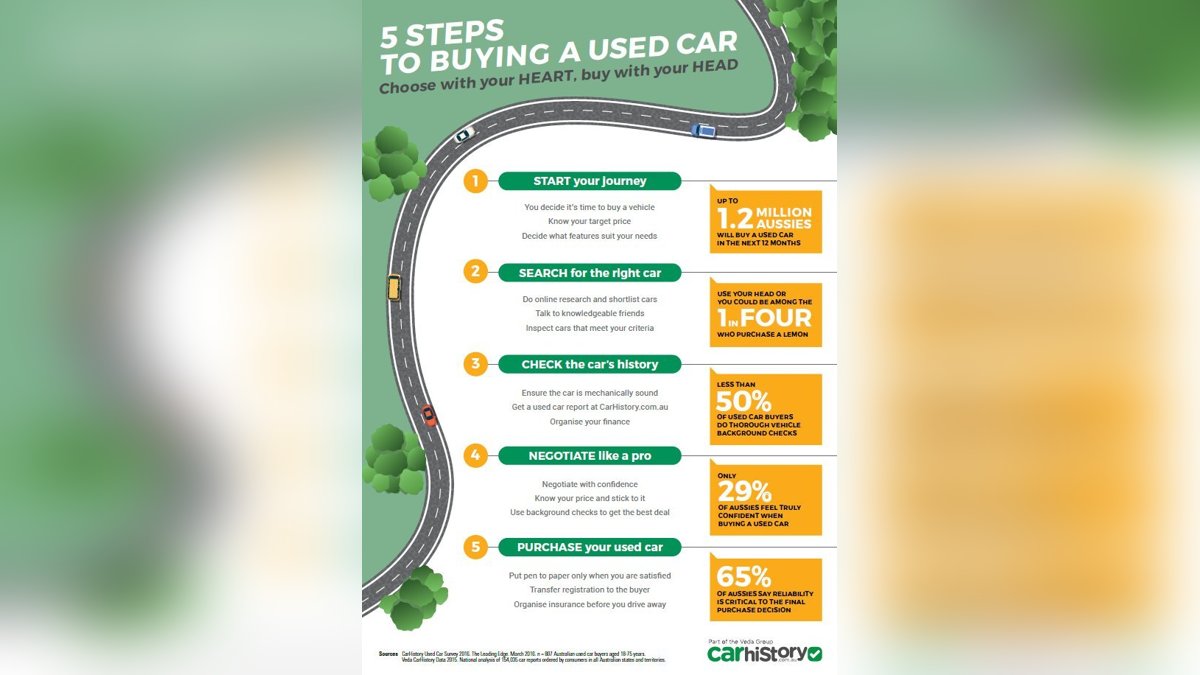

Buying a car is one of the largest financial decisions most people make, yet many buyers walk onto dealership lots unprepared. A strategic approach to car buying can save you thousands of dollars and prevent years of regret. The process breaks down into several distinct stages: research and budgeting, financing, finding the right vehicle, test driving, negotiation, and finalizing the paperwork. Each stage requires its own set of skills and knowledge, and skipping any one of them can lead to costly mistakes. This guide walks through the complete car buying journey, equipping you with the information you need to make a confident, informed purchase whether you are buying new or used.

Setting Your Budget the Right Way

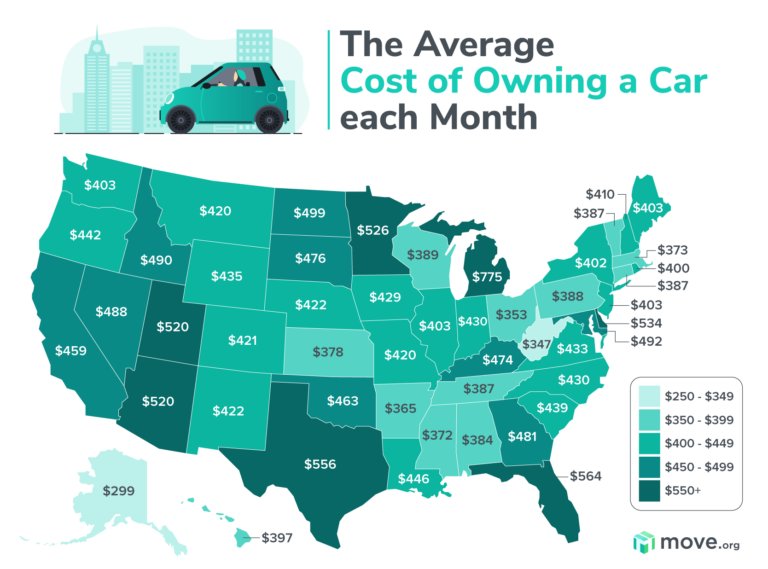

Before you open a single listing or visit a dealership, you need a clear budget. The 20/4/10 rule remains one of the most practical frameworks: put at least 20 percent down, finance for no more than four years, and keep your total monthly car expenses including insurance and fuel under 10 percent of your gross monthly income. Many buyers focus solely on the monthly payment, which is exactly what dealership finance managers want you to do. A low monthly payment stretched over 72 or 84 months might look affordable but traps you in negative equity for years. Calculate the total cost of ownership, not just the sticker price or monthly note. Factor in insurance premiums, which vary dramatically between models, as well as fuel or charging costs, annual registration fees, and expected maintenance. A car that costs less upfront can end up more expensive over five years if it requires premium fuel, expensive parts, or high insurance rates.

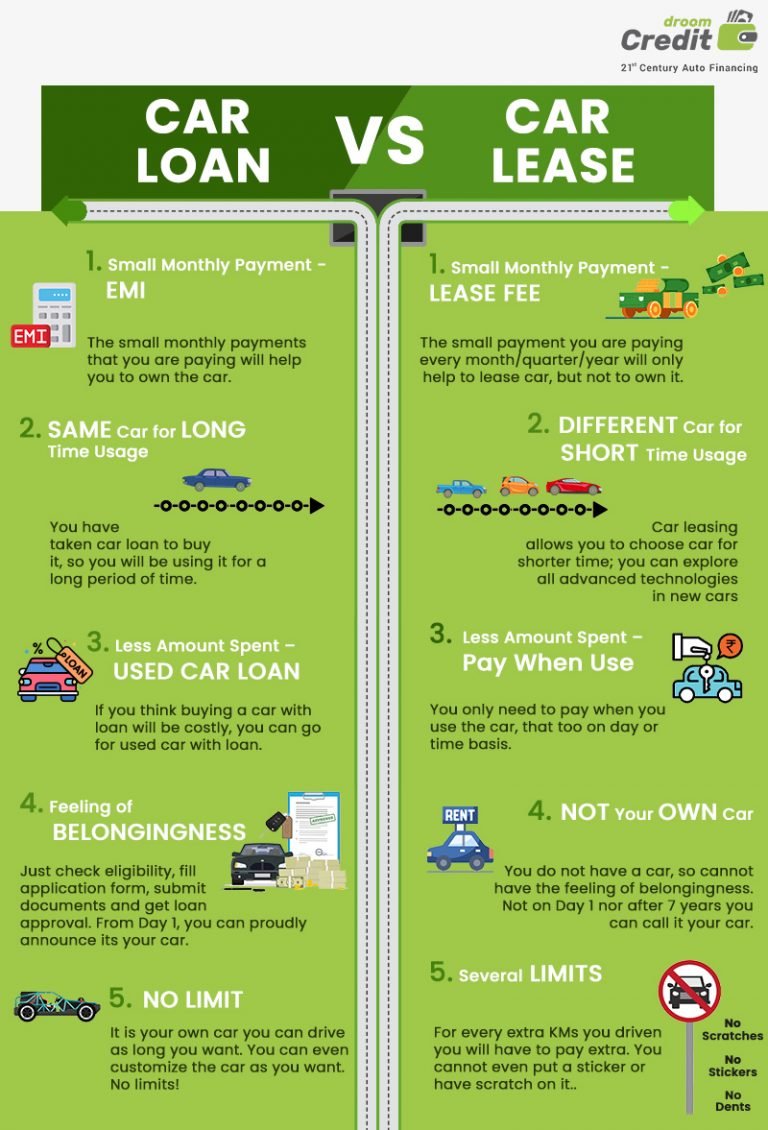

Financing: Pre-Approval Before You Shop

One of the most powerful tools in a car buyer's arsenal is a pre-approved loan from a bank, credit union, or online lender. Walking into a dealership with pre-approval gives you a baseline interest rate and shifts the negotiation from monthly payment to the actual price of the vehicle. Credit unions often offer the most competitive rates, sometimes a full percentage point below what dealership financing advertises. Dealership financing is not inherently bad, but the finance office is a profit center where interest rates can be marked up, extended warranties are pushed aggressively, and add-ons like fabric protection and VIN etching appear on the contract without clear disclosure. Having your own financing ready creates a fallback position. If the dealer can beat your rate, great. If not, you already have a loan locked in. Check your credit score before applying, correct any errors on your report, and avoid applying for multiple loans within a short window since each hard inquiry can temporarily lower your score by a few points.

New vs. Certified Pre-Owned vs. Used

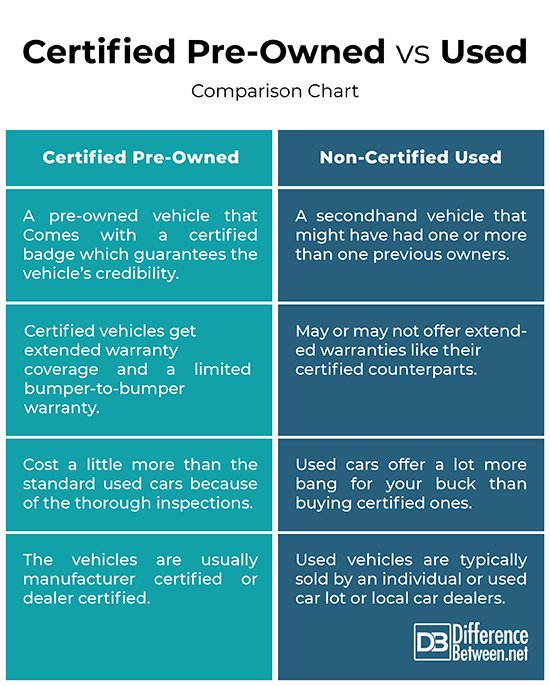

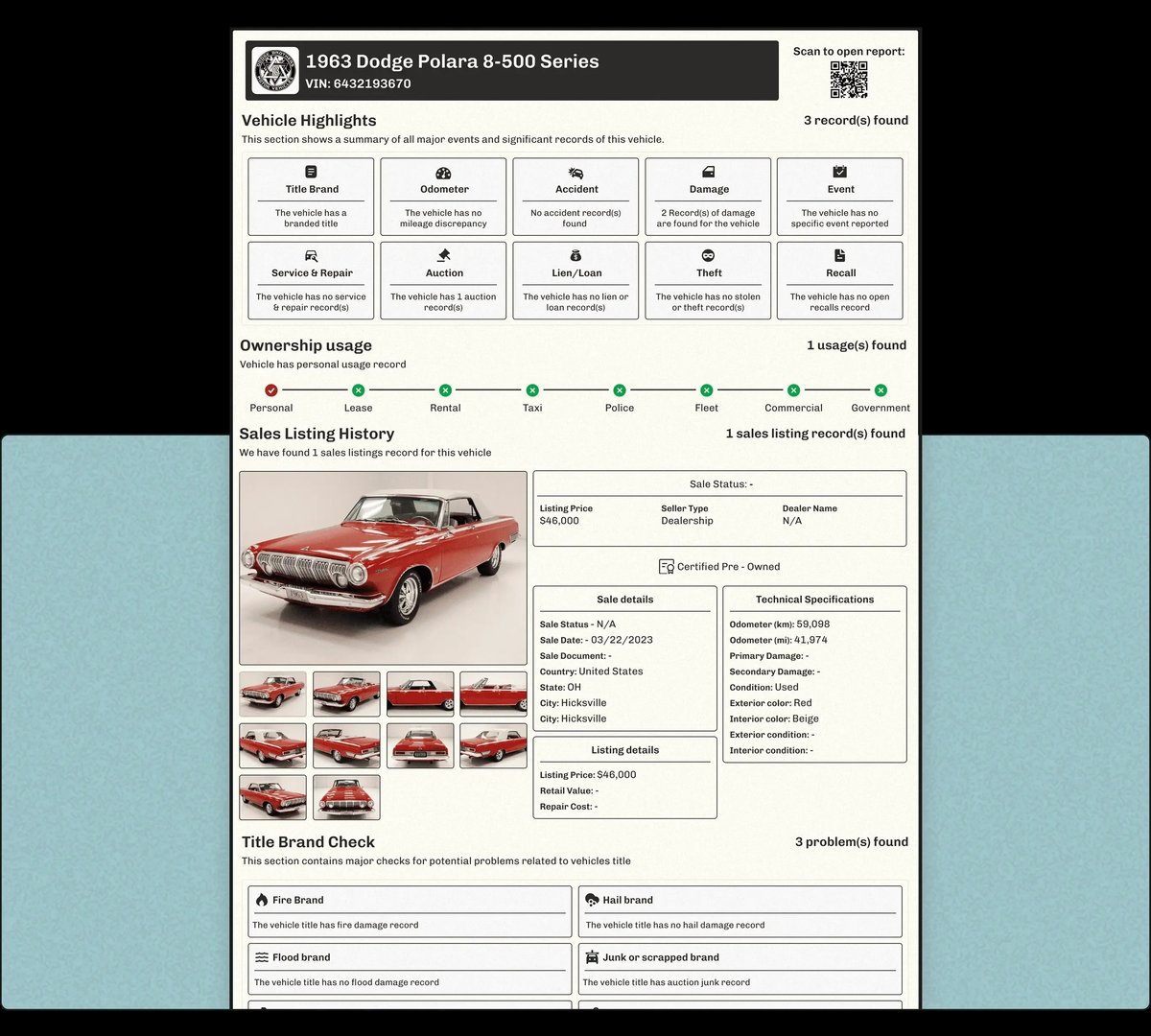

New cars come with the latest safety technology, full factory warranties, and that unmistakable new-car smell, but they also depreciate roughly 20 percent the moment you drive off the lot and lose about 60 percent of their value over the first five years. Certified pre-owned vehicles offer a middle ground: they are typically two to four years old, have passed a manufacturer inspection, and include an extended warranty backed by the automaker. The premium for CPO status usually ranges from one to three thousand dollars over a comparable non-certified used car, which is often worth it for the warranty coverage alone. Traditional used cars offer the lowest purchase price but require the most diligence. A pre-purchase inspection by an independent mechanic is non-negotiable when buying used, even if the car looks clean and the seller seems honest. Always run a vehicle history report through Carfax or AutoCheck to check for accidents, title issues, flood damage, and odometer discrepancies. A single undisclosed accident can reduce a car's value by ten to thirty percent.

The Test Drive and Inspection

A proper test drive goes beyond a quick loop around the block. Test the car in conditions that reflect your daily driving: highway merging, stop-and-go traffic, parallel parking, and rough pavement if your area has it. Listen for unusual noises from the engine, transmission, suspension, and brakes. Check that every electronic feature works, from the infotainment screen to the heated seats to the backup camera. Pay attention to seat comfort and driving position since you will spend hundreds of hours in this seat. For used cars, bring a checklist: check tire tread depth with a penny test, look for uneven wear that indicates alignment issues, inspect under the oil cap for sludge that suggests neglected maintenance, and check for paint overspray that might reveal body repairs. Bring a friend or family member who is not emotionally invested in the purchase; they will notice things you overlook in your excitement. If anything feels off during the test drive, walk away. There will always be another car.

Negotiation and Closing the Deal

Negotiation is where many buyers leave money on the table. Research the market value of your target vehicle using multiple sources before you walk in. Know the invoice price, the average transaction price in your region, and any manufacturer incentives or rebates currently available. Negotiate the out-the-door price, which includes the vehicle price plus taxes, title, registration, and all fees, rather than the monthly payment. Dealers sometimes try to bundle negotiations by asking what monthly payment you want while hiding a higher vehicle price inside a longer loan term. If the dealer presents a worksheet with numbers you do not recognize, ask for a line-by-line explanation of every charge. Common junk fees include documentation fees far above the state average, advertising fees, and dealer prep charges. Be prepared to walk away at any point. The person most willing to leave the table holds the negotiating power. Once you agree on a price, review the contract carefully before signing. Ensure the numbers match what was discussed and that no extras were added without your knowledge. A car purchase is a binding legal agreement, not just a handshake deal.

Beyond the transaction itself, smart buyers think ahead to insurance, extended warranties, and gap coverage. Insurance should be quoted before you commit to a specific vehicle, as premiums can vary by hundreds of dollars per year between models that cost the same to purchase. Extended warranties sold by dealerships are almost always overpriced relative to the expected repair costs they cover. Manufacturer-backed extended service contracts purchased online from competing dealers are often half the price for identical coverage. Gap insurance, which covers the difference between your loan balance and the car's actual cash value if it is totaled, is worth considering if you put down less than 20 percent. However, gap coverage from your auto insurer typically costs a fraction of what the dealership finance office charges. Spend a few hours researching these post-purchase items before you sit down to sign, and you will save hundreds more on top of the savings from negotiating the vehicle price itself.