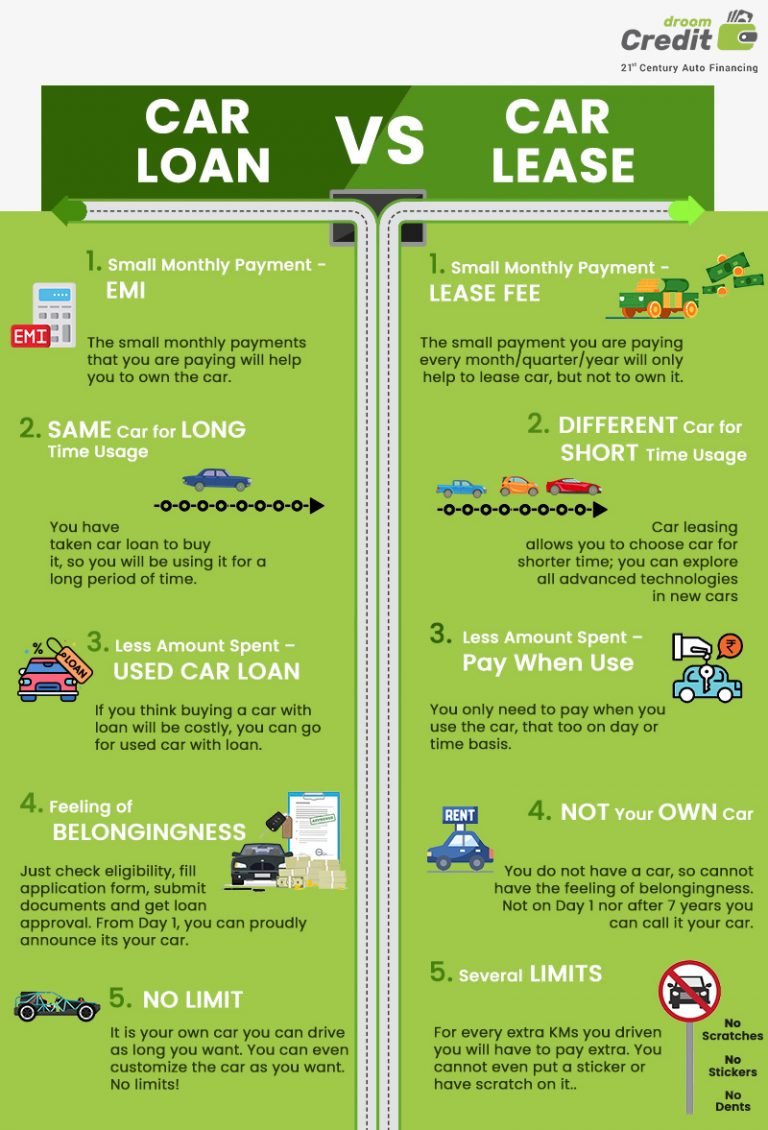

Deciding whether to finance a car with a loan or lease it is one of the most consequential financial choices a driver makes. In 2026, with average new-car transaction prices hovering around $48,000 and interest rates still elevated from recent highs, the gap between these two paths has widened. A loan builds equity but demands higher monthly payments; a lease offers lower payments but comes with strict mileage caps and no ownership at the end. This guide breaks down the real numbers, hidden fees, tax implications, and scenarios where each option wins--so you can choose the path that saves the most money for your specific situation.

According to Edmunds data, the average monthly payment for a new-car loan in Q1 2026 was $734, while the average lease payment was $586--a difference of $148 per month. However, lease fees and mileage penalties can erase that savings in just two years.

1. Monthly Payment Breakdown: Loan vs Lease with Real 2026 Numbers

The most visible difference between a loan and a lease is the monthly payment. For a $45,000 vehicle with a 60-month loan at 6.5% APR (the average for prime borrowers in early 2026), the monthly payment is approximately $880. The same vehicle leased for 36 months with a 58% residual value and a money factor equivalent to 5.0% APR results in a monthly payment of about $620. That's a $260 monthly difference--$9,360 over three years.

However, the loan payment includes principal repayment that builds equity. After three years of loan payments, you would have paid $31,680 and owe roughly $18,900 on the loan, but the car's market value (assuming 15% annual depreciation) is about $27,600. Your equity is approximately $8,700. With a lease, you have zero equity at the end--you simply return the car. The lower lease payment is essentially paying for the depreciation during the lease term plus interest and fees.

For a $35,000 vehicle, the numbers shift. A 60-month loan at 6.5% yields a $685 monthly payment. A 36-month lease with 55% residual and 5.0% money factor yields about $480 per month. The $205 monthly savings on the lease totals $7,380 over three years, but you walk away with nothing. The loan builds roughly $6,500 in equity after three years. The net advantage depends on how long you keep the car and what you do with the money saved each month.

2. Hidden Fees: Acquisition, Disposition, and Mileage Penalties

Leases come with a suite of fees that loans do not. The acquisition fee, typically $650-$1,000, is charged by the leasing company to set up the contract. Some dealers roll this into the monthly payment, but it still adds to your total cost. The disposition fee, usually $350-$500, is charged when you return the vehicle at lease end. If you lease another car from the same manufacturer, this fee is often waived, but it's still a cost you must plan for.

Mileage penalties are the biggest hidden cost. Most leases allow 10,000-12,000 miles per year. Exceeding that triggers a charge of $0.15-$0.25 per mile. If you drive 15,000 miles per year on a 12,000-mile lease, you'll owe $450-$750 annually in penalties. Over a three-year lease, that's $1,350-$2,250. For high-mileage drivers, a loan is almost always cheaper because there's no mileage restriction.

Loans have their own hidden costs: origination fees (rare but possible), prepayment penalties (uncommon but check your contract), and higher insurance requirements. Leases require gap insurance and often demand higher liability limits, which can increase your annual premium by $200-$400. Always factor these into your total cost comparison.

3. When Leasing Makes Financial Sense--and When It Doesn't

Leasing is financially optimal in three specific scenarios. First, if you change cars every 2-3 years and want the latest technology, safety features, or electric vehicle range. Leasing transfers depreciation risk to the lender. In 2026, with EV values dropping faster than expected due to rapid battery tech improvements, leasing protects you from negative equity. Second, if you have a business and can deduct lease payments as an operating expense (see section 4). Third, if you have limited cash for a down payment--leases often require $0-$2,000 down versus 10-20% for a loan.

Leasing is a bad deal when you drive more than 12,000 miles per year, want to customize your vehicle, or plan to keep the car for 5+ years. The cumulative cost of leasing three consecutive 3-year terms ($620/month × 36 months × 3 = $66,960) far exceeds the cost of a single 72-month loan ($880/month × 72 = $63,360) for the same $45,000 car--and you own the car after the loan. Additionally, if you damage the car beyond normal wear and tear, you'll face hefty charges at lease return. A single dent or scratch can cost $500-$1,500 in repair bills.

For electric vehicles in 2026, leasing is particularly attractive because federal tax credits (up to $7,500) often apply to leases even when the vehicle doesn't qualify for the purchase credit. Many manufacturers pass this savings through as a capitalized cost reduction, lowering your monthly payment by $100-$200. If you're considering an EV, run the lease numbers carefully--they often beat loan payments by a wider margin than gas cars.

4. Tax Implications and Business Write-Off Considerations

For personal use, neither loan interest nor lease payments are tax-deductible. However, for business use, the rules differ significantly. If you use the vehicle at least 50% for business, you can deduct lease payments proportionally. In 2026, the IRS standard mileage rate is $0.67 per mile for business use, which often yields a larger deduction than actual lease costs. For a leased vehicle, you can deduct the business-use percentage of each lease payment. For example, if you use the car 70% for business, you deduct 70% of $620 = $434 per month.

With a loan, you can deduct the business-use percentage of interest payments plus depreciation under Section 179 or bonus depreciation. In 2026, the Section 179 limit for vehicles over 6,000 lbs GVWR (SUVs and trucks) is $28,900. For passenger cars, the limit is lower--around $12,200 for the first year. Bonus depreciation is being phased down to 60% in 2026. A business that buys a $45,000 SUV might deduct $28,900 in year one plus 60% of the remaining $16,100, totaling $38,560 in first-year deductions. That's a powerful tax advantage that leasing cannot match.

For self-employed individuals and small business owners, leasing offers simplicity: you deduct the actual lease payment without tracking depreciation. But if you need maximum first-year write-offs, buying with a loan and using Section 179 is superior. Consult a CPA to model your specific tax situation--the difference can be thousands of dollars annually.

5. Total Cost of Ownership: Which Option Saves More Over 3, 5, and 7 Years

To determine which option saves more money, you must calculate total cost of ownership (TCO) including depreciation, interest, fees, insurance, maintenance, and taxes. For a $45,000 vehicle kept three years: a loan costs $31,680 in payments plus $1,200 in extra insurance and $500 in maintenance = $33,380 total outlay, minus $8,700 equity = net cost of $24,680. A lease costs $22,320 in payments plus $1,000 acquisition fee, $450 disposition fee, $600 extra insurance, and $300 maintenance = $24,670 total outlay, with zero equity. The lease saves $10 over three years--essentially a tie, but the lease requires less cash upfront.

Over five years: the loan is paid off after 60 months at $52,800 total payments, plus $2,000 insurance and $1,500 maintenance = $56,300 total, with the car worth about $18,000 (assuming 60% depreciation over 5 years). Net cost: $38,300. Two consecutive 3-year leases (6 years) cost $44,640 in payments plus $2,000 in fees and $1,200 insurance = $47,840, with zero equity. The loan saves $9,540 over six years. Over seven years: the loan is long paid off, and you own a car worth $12,000 with no payments. Leasing for seven years (two 3-year leases plus a 1-year extension) costs $51,520 in payments plus fees--far more expensive.

The breakeven point is around 3.5 years. If you keep the car longer, buying wins. If you switch every 2-3 years, leasing can be cheaper when you factor in lower payments and no negative equity risk. In 2026, with interest rates still above 6%, the math slightly favors leasing for short-term ownership, but buying remains the long-term wealth-building choice.